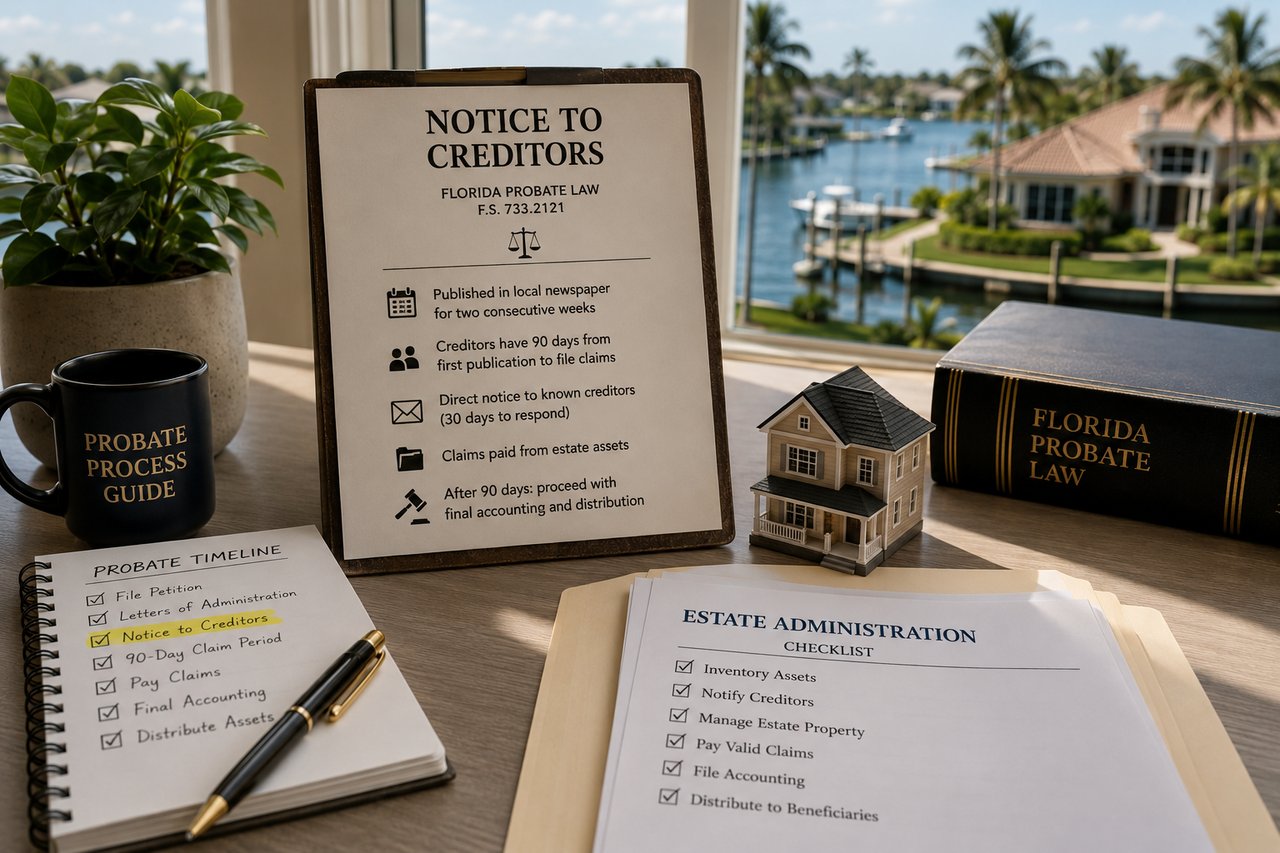

The Notice to Creditors is a legally required step in Florida formal probate administration that triggers a 90-day window during which creditors can file claims against the estate. It directly affects how quickly the estate can be closed and assets distributed — including the real estate. Here is what it means practically and how to work within it.

Understanding the Notice to Creditors Before You Plan Your Timeline

When families contact me about selling an inherited property in Southwest Florida, one of the most common timeline surprises comes from the Notice to Creditors requirement. They assumed — reasonably — that once the personal representative had Letters of Administration and the property was ready to sell, the process would move quickly toward closing. Then their probate attorney explains the Notice to Creditors, and suddenly there is a mandatory waiting period of at least 90 days that nobody accounted for.

Understanding this requirement from the beginning — before you make plans about what to do with the sale proceeds — will save you significant frustration. My legal background gives me a solid grasp of where this fits in the overall probate timeline, and it is something I explain to every family I work with on a probate property in Lee or Collier County.

What the Notice to Creditors Actually Is

The Legal Framework

Florida Statute 733.2121 requires that the personal representative of an estate publish a Notice to Creditors in a locally circulating newspaper — one that is in or nearest to the county where the probate is pending. This publication must happen within 30 days of the appointment of the personal representative, and it must run for two consecutive weeks.

The Notice to Creditors informs any creditors of the decedent — credit card companies, medical providers, contractors, banks, former business partners, or anyone else who might have a valid claim against the estate — that the estate is in administration and that they must file a claim within the statutory deadline if they want to be paid.

The 90-Day Claim Period

Once the Notice to Creditors is first published, creditors have 90 days to file a claim against the estate. This is a hard deadline — creditors who fail to file within the 90-day window are generally barred from making claims against the estate, with certain exceptions for claims that could not reasonably have been known within that period.

This 90-day window is one of the main reasons that Florida formal administration takes a minimum of several months even in straightforward cases. You cannot close the estate — cannot make final distributions to beneficiaries — until the creditor claim period has run and all valid claims have been addressed.

Direct Notice to Known Creditors

In addition to the newspaper publication, the personal representative must also provide written direct notice to any known creditors of the decedent — creditors whose names and addresses are reasonably ascertainable from the estate's records. Known creditors must be notified directly and have 30 days from the date of that notice to file a claim (or the 90-day newspaper publication period, whichever is later).

Common known creditors in estate administration include mortgage lenders, healthcare providers who treated the decedent, the IRS if there are outstanding tax obligations, and any individuals who had written agreements with the decedent.

How This Affects the Property Sale Timeline

Can You Sell During the Creditor Claim Period?

Yes — and this is an important point. The Notice to Creditors requirement does not prohibit the sale of real estate during the claim period. The personal representative can list, market, negotiate, and close on the sale of estate real property while the creditor claim period is running, provided they have the authority to do so under the Letters of Administration.

What cannot happen during the creditor period is the final distribution of net proceeds to beneficiaries. The net sale proceeds go into the estate account, where they sit until the creditor claim period has closed, all valid claims have been paid, and the court approves the final accounting and distribution.

This is actually an important strategic opportunity: if you start the sale process early — ideally at the same time the Notice to Creditors is being published — the property can be under contract or even closed before the 90-day period ends, and the proceeds will be ready to distribute immediately once the legal timeline allows.

What Happens if Claims Are Filed

If creditors file claims during the 90-day window, the personal representative must evaluate each claim and either accept it (pay it from estate assets) or object to it (file a formal objection and potentially litigate the claim). Valid claims reduce the net estate available for beneficiary distribution. Invalid claims that are successfully objected to do not.

For most residential estate sales in SWFL, the creditor claims process is routine — a mortgage lender who gets paid at closing, standard medical bills, perhaps a credit card balance. In more complex estates with business interests or significant debt, the creditor process becomes more involved and requires closer attorney management.

A Common Misunderstanding: Homestead Property

One important nuance that affects many SWFL families: Florida's homestead protection extends into probate in specific ways. The decedent's homestead property — the primary residence — has special treatment under Florida law. It descends directly to certain heirs outside of the normal estate administration process in some circumstances, and it is generally not subject to the claims of most estate creditors (with exceptions for certain secured debts like the mortgage and certain specific statutory claims).

This does not mean the homestead property bypasses the probate process entirely — in many cases it still needs to go through probate to clear the title for sale. But the homestead protection can affect what creditors can reach and how the proceeds of a homestead sale are treated. Your probate attorney will navigate this distinction for your specific situation.

My Role in the Probate Sale Timeline

I coordinate the real estate sale timeline to align with the legal process as efficiently as possible. That means starting the pre-listing preparation — cleaning, repairs, photography, pricing analysis — during the Notice to Creditors period so the property is ready to go live on MLS as soon as the timing is right. Rather than the real estate waiting for the legal process, both move in parallel, and the result is a faster overall resolution for the family.

Ready to make your move in Southwest Florida? Let's talk.

Whether you're buying, selling, investing, managing an estate, or just want an honest read on the market — I'm here for that conversation.

Call or text: 727.638.1704

Email: [email protected]

Or reach out at theabreugroup.com

— Daniel

Frequently Asked Questions

Q: What if no creditors file during the 90-day period?

If no creditors file valid claims during the 90-day Notice to Creditors period, the estate is not required to pay any unsecured claims beyond what was filed, and the personal representative can proceed with the final accounting and distribution to beneficiaries. This is the most common outcome in straightforward residential estates — most creditors have already received payment or the debts are already satisfied.

Q: Does the mortgage company get paid through the creditor claim process?

No — the mortgage is a secured debt attached to the real property, not an unsecured claim against the estate. The mortgage is paid off at the closing of the real estate sale from the gross proceeds, just as it would be in any standard property sale. The creditor claim process deals with unsecured debts and other claims against the general estate assets.

Q: What if we do not know all of the decedent's creditors?

The personal representative is required to make a reasonable effort to identify and notify known creditors. Unknown creditors are addressed through the newspaper publication — if they do not respond within the 90-day window after publication, their claims are generally barred. The personal representative is not held liable for unknown creditors they could not have reasonably discovered through diligent search.

Q: Can the 90-day creditor period be shortened?

No — the 90-day Notice to Creditors period is a statutory requirement in Florida formal administration and cannot be shortened by agreement or court order. It is one of the fixed elements of the Florida probate timeline that everyone — families, attorneys, and real estate professionals — must plan around.

This post is intended for general educational and informational purposes only and does not constitute legal advice. The information provided here reflects general principles of Florida probate law and should not be relied upon as a substitute for advice from a licensed Florida attorney. Every estate is different, and the specific facts of your situation may lead to different legal outcomes. If you are dealing with probate, estate administration, or any related legal matter, please consult with a qualified Florida probate attorney before taking action.