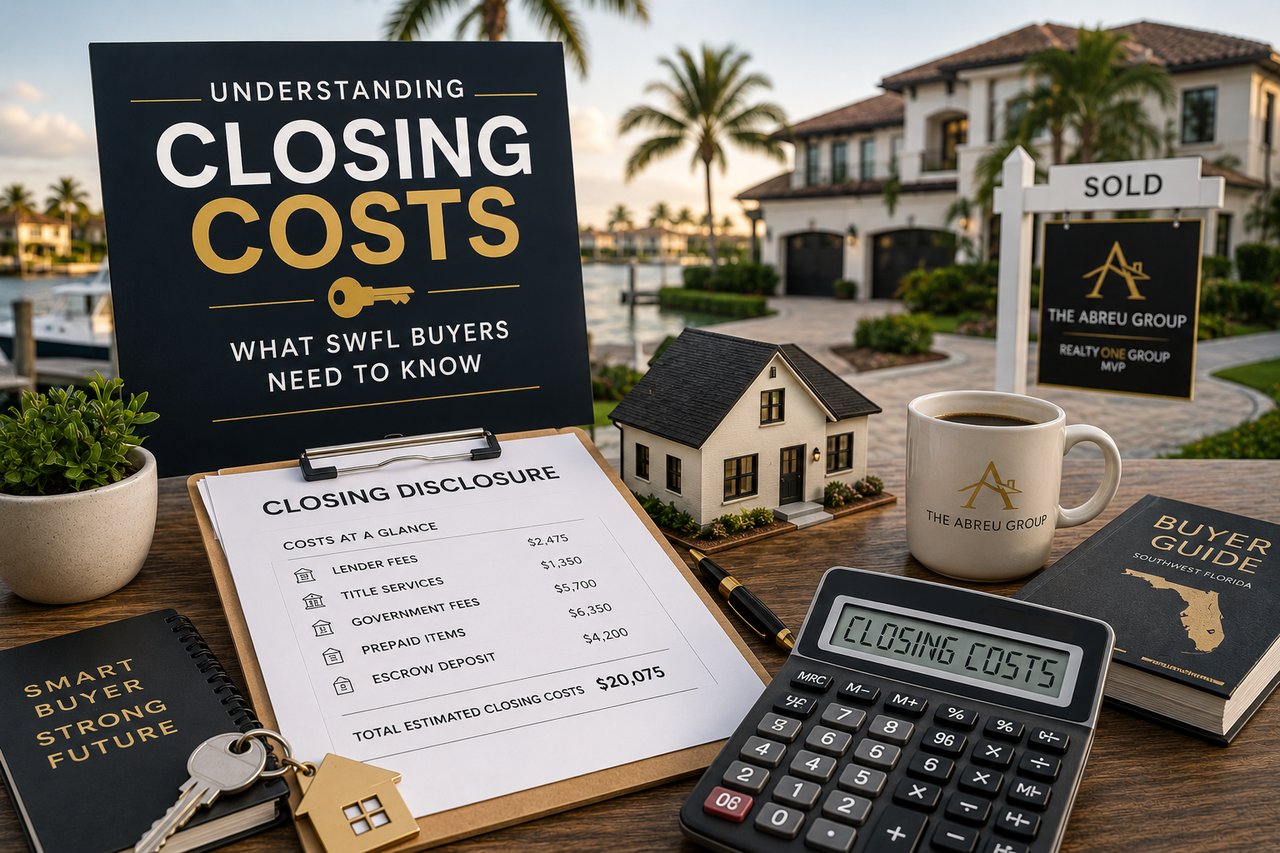

Florida closing costs typically run 2 to 4 percent of the purchase price on top of your down payment — and for SWFL buyers, the specific line items often include a few surprises. Here is a complete breakdown of what you will see on the closing disclosure, what is negotiable, and how to budget accurately so nothing catches you off guard on closing day.

Nobody Likes Surprises at the Closing Table

I have sat at a lot of closing tables over the years, and one of the most consistent sources of buyer stress is the gap between what they budgeted for closing costs and what they actually owe. The problem is almost never that the costs were hidden — they are all disclosed on the Loan Estimate and the Closing Disclosure that federal law requires lenders to provide. The problem is that buyers often focus only on the down payment number and treat closing costs as an afterthought.

In Southwest Florida, where the purchase prices are higher than the national average and certain Florida-specific costs add line items that buyers from other states are not used to, understanding the full closing cost picture before you make an offer is genuinely important. Here is the complete breakdown.

Lender Fees: What Your Mortgage Costs to Obtain

Origination and Underwriting Fees

Your lender charges fees for processing and underwriting your loan. These typically include an origination fee (sometimes expressed as a percentage of the loan amount, sometimes as a flat fee), an underwriting fee, and various administrative charges. On a $500,000 loan, total lender fees commonly run $1,500 to $3,000 depending on the lender and the loan type. Shopping multiple lenders and comparing the Loan Estimate documents is the most effective way to minimize this category.

Discount Points

Discount points are optional — you pay them upfront to buy down your interest rate. Each point is 1 percent of the loan amount. Whether paying points makes sense depends on how long you plan to hold the loan before refinancing. In the current rate environment, many buyers are choosing not to pay points because they expect to refinance when rates drop — though this expectation is not guaranteed.

Appraisal Fee

Your lender will require an appraisal of the property to confirm it is worth at least the purchase price before funding the loan. In SWFL, residential appraisals typically cost $500 to $800 for standard single-family homes and can run higher for luxury properties or complex waterfront situations where fewer comparables are available.

Title-Related Costs: Florida's Unique Structure

Title Search and Examination

The title company conducts a search of the public records to identify any liens, encumbrances, or title defects affecting the property. The title search fee is typically $150 to $300.

Title Insurance — Owner's and Lender's Policies

As covered in a recent post, Florida custom has the seller paying for the owner's title insurance policy and the buyer paying for the lender's title insurance policy. The lender's policy premium is based on the loan amount and is set by the Florida Office of Insurance Regulation — on a $400,000 loan, expect approximately $2.50 per $1,000 of coverage, so roughly $1,000. The owner's policy (paid by the seller) is calculated on the purchase price at a similar rate.

Title Company Closing and Settlement Fees

The title company charges for conducting the closing — the settlement fee, escrow fee, or closing fee. In SWFL, this typically runs $500 to $900 for a standard residential transaction. There may also be courier fees, notary fees, and document preparation fees that together add another $100 to $200.

Government Recording and Transfer Costs

Documentary Stamp Tax on the Deed

Florida charges a documentary stamp tax on the deed when real property is transferred. The rate is $0.70 per $100 of purchase price (or $0.60 per $100 in Miami-Dade County). On a $500,000 purchase, the doc stamp on the deed is $3,500. In Florida, the seller customarily pays the doc stamp on the deed — but this is a negotiable custom, not a legal requirement.

Documentary Stamp Tax on the Note

Florida also charges a documentary stamp tax on the mortgage note itself. The rate is $0.35 per $100 of the loan amount. On a $400,000 mortgage, this is $1,400. This cost is typically the buyer's responsibility.

Intangible Tax on the Mortgage

Florida charges an intangible tax on new mortgages at a rate of $0.002 per dollar of the loan amount (0.2 percent). On a $400,000 mortgage, this is $800. Also typically the buyer's responsibility.

Recording Fees

The county charges fees to record the deed and mortgage in the public record. Lee and Collier County recording fees typically run $10 to $20 per document with a first-page fee plus a per-additional-page fee. Total recording fees for a standard transaction usually run $100 to $200.

Prepaid Items and Escrow Deposits: The Category That Surprises Buyers Most

Prepaid Homeowners Insurance

Your lender will require proof of homeowners insurance before closing, and the first year's premium is typically paid upfront at closing. In SWFL, where homeowners insurance runs $4,000 to $12,000+ per year, this can be a significant upfront cost that buyers from other states drastically underestimate.

Prepaid Flood Insurance

If the property is in a flood zone requiring flood insurance, the first year's flood insurance premium is also typically paid at closing. Budget $2,000 to $6,000+ depending on the flood zone and property characteristics.

Prepaid Mortgage Interest

Your lender collects interest from the closing date through the end of the month at closing. If you close on July 10th, you prepay 21 days of interest at closing. At a 6.75 percent rate on a $400,000 loan, that is approximately $1,850.

Escrow Account Setup — Taxes and Insurance Reserves

If your lender requires an escrow account (most do on conventional loans), they will collect reserves at closing to establish the account. Typically two to three months of property taxes and two months of homeowners and flood insurance are collected upfront. On a SWFL property with $6,000 in annual taxes, $8,000 in homeowners insurance, and $4,000 in flood insurance, the escrow setup reserves can total $3,500 to $5,000.

HOA-Related Costs

Many SWFL properties are in HOA communities, and closing on these properties involves additional fees:

- HOA estoppel fee: $100 to $250 — the fee for the HOA to certify the current state of dues, fees, and any violations (typically seller-paid but negotiable)

- HOA transfer fee: $50 to $500 depending on the community — charged to process the ownership transfer in the HOA's records (typically buyer-paid)

- HOA capital contribution or initiation fee: some communities charge new buyers a one-time capital contribution fee, which can range from a few hundred to several thousand dollars

- CDD fee proration if applicable: if the property is in a CDD, the annual CDD assessment may be prorated at closing

Total Closing Cost Budget

For a SWFL buyer purchasing a $500,000 home with 20 percent down ($100,000 down payment), a realistic total closing cost estimate — including lender fees, title costs, government taxes, prepaid items, and escrow setup — runs approximately $18,000 to $28,000 on top of the down payment. On higher-priced properties the absolute dollar amount increases, though some categories scale with the loan amount rather than the purchase price.

The practical implication: SWFL buyers should budget 3 to 5 percent of the purchase price for total out-of-pocket costs at closing in addition to their down payment, with the higher end of that range more likely for properties in flood zones with significant insurance costs.

Ready to make your move in Southwest Florida? Let's talk.

Whether you're buying, selling, investing, managing an estate, or just want a straight read on the market — I'm here for that conversation.

Call or text: 727.638.1704

Email: [email protected]

Or reach out at theabreugroup.com

— Daniel

Frequently Asked Questions

Q: Can closing costs be rolled into the mortgage in Florida?

Generally no — conventional loans do not allow closing costs to be added to the loan amount beyond the purchase price. However, sellers can agree to pay a portion of your closing costs as a concession in the purchase contract. Lender credits (where you accept a slightly higher rate in exchange for the lender covering some fees) are another option. In a buyer-favorable market, asking for seller concessions toward closing costs is a common and often successful negotiating strategy.

Q: Who pays closing costs in a Florida real estate transaction?

Florida has customary practices for who pays what, though most items are technically negotiable. Sellers customarily pay: real estate commissions, documentary stamp tax on the deed, title search, and the owner's title insurance policy. Buyers customarily pay: documentary stamp tax on the note, intangible tax on the mortgage, lender's title insurance, appraisal, prepaid items, and escrow setup. In a buyer's market, sellers may agree to contribute to buyer closing costs as an incentive.

Q: Are closing costs tax-deductible in Florida?

Some closing costs have tax implications. Mortgage interest prepaid at closing is typically deductible. Discount points paid to reduce the interest rate may be deductible in the year of purchase. Property taxes prepaid at closing are deductible in the year paid. However, most other closing costs — title insurance, lender fees, government taxes — are not deductible. Consult with a CPA for guidance specific to your situation.

Q: How do I get an accurate estimate of my closing costs before making an offer?

Your lender is required to provide a Loan Estimate within three business days of receiving a loan application, which includes a detailed estimate of your closing costs. Getting a Loan Estimate from two or three lenders before you make an offer — not after — gives you an accurate comparison and lets you budget properly. Since I am a title company as well, I also walk every buyer client through a rough closing cost estimate before we submit an offer so there are no surprises.