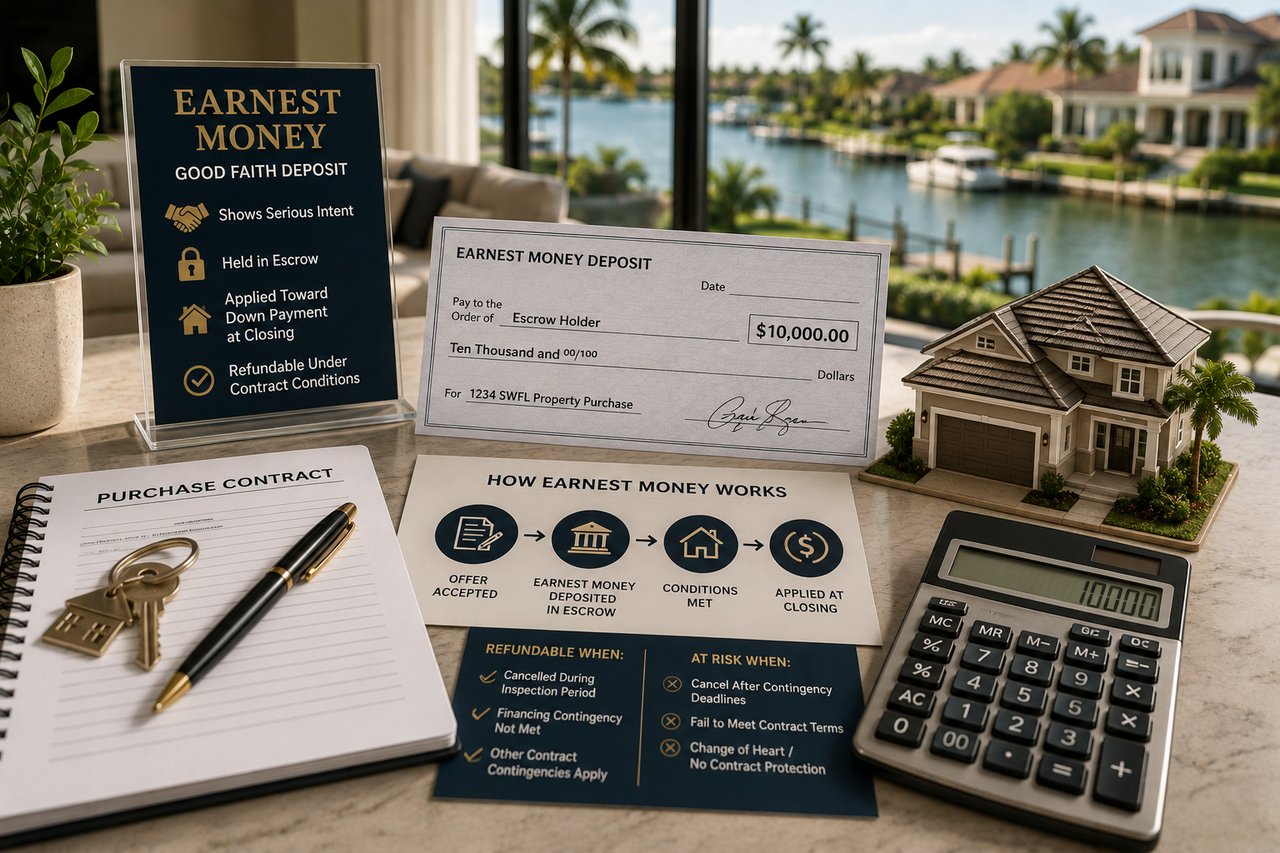

Earnest money is a good-faith deposit that a buyer puts down when making an offer on a home in Florida — it signals serious intent and is typically held in escrow by the title company or broker. The amount, the timeline for depositing it, and the conditions under which it is refundable or forfeited are all things every Florida buyer needs to understand before signing a contract.

What Earnest Money Actually Is

When you make an offer to purchase a home in Florida, you are not just submitting paperwork — you are making a financial commitment that demonstrates to the seller you are serious. That commitment takes the form of an earnest money deposit, sometimes called an escrow deposit or good faith deposit, that you agree to put into escrow within a specific timeframe after the contract is accepted.

The earnest money is not a down payment — it does not go directly to the seller at this stage. It is held in a neutral escrow account, typically by the title company or occasionally by a real estate brokerage. If the transaction closes successfully, the earnest money is credited toward your down payment and closing costs. If it does not close, what happens to the money depends entirely on the reason the deal fell through and the specific terms of the contract.

How Much Earnest Money Is Typical in SWFL?

The Standard Range

In Southwest Florida, earnest money deposits typically run 1 to 3 percent of the purchase price, though the range can go higher in competitive situations or for luxury properties. Here is what that looks like in real dollar terms:

- $300,000 to $500,000 purchase price: typical earnest money of $3,000 to $10,000

- $500,000 to $1,000,000 purchase price: typical earnest money of $10,000 to $25,000

- $1,000,000 to $3,000,000 purchase price: typical earnest money of $25,000 to $75,000

- $3,000,000+: earnest money varies widely but often runs 3 to 5 percent, sometimes more for highly competitive offers

When to Put Down More

In certain situations, a larger earnest money deposit strengthens your offer meaningfully. If you are competing against other buyers — particularly in the under-$600K segment in Fort Myers or Cape Coral where multiple-offer situations still occur — a larger earnest money deposit signals financial strength and commitment. For sellers who have had buyers walk away previously, a larger deposit provides reassurance. And in cash purchase situations, where there are fewer contingencies protecting the seller, a more substantial earnest money deposit is often expected.

The Deposit Timeline in Florida

The Florida Realtors standard contract specifies that the earnest money deposit must be delivered to escrow within 3 business days of the effective date of the contract (the date the last party signs). Missing this deadline — even by a day — can give the seller grounds to declare the buyer in default. In competitive markets or with motivated sellers, I always advise clients to initiate the wire transfer the same day the contract is signed rather than waiting the full three days.

The title company or holding broker will provide wire instructions and confirm receipt. Keep documentation of the wire transfer — you will need it to confirm the deposit at closing when it is applied to your costs.

When Is Earnest Money Refundable?

During the Inspection Period

The Florida standard contract includes an inspection period — typically 10 to 15 days — during which the buyer has the right to inspect the property and cancel the contract for any reason whatsoever, receiving a full refund of the earnest money. This is the buyer's most powerful protection period. If you cancel for any reason during the inspection period and in the proper manner, your earnest money comes back to you.

Financing Contingency

If your contract includes a financing contingency — which standard contracts do, unless waived — and you are unable to obtain financing approval despite making good-faith efforts to do so, you are generally entitled to a refund of your earnest money. The financing contingency has a deadline (typically 30 to 45 days after the effective date) and specific requirements for documentation and notice — if you do not follow the proper process, you may lose the deposit even if your loan was legitimately denied.

Other Contingencies

Contracts may include additional contingencies — appraisal contingencies, sale of prior property contingencies, and others — each of which has its own conditions under which the earnest money is refundable. Understanding exactly what contingencies your contract contains and what the requirements are to exercise them properly is critical. I review this with every buyer client before we sign anything.

When Is Earnest Money at Risk?

Your earnest money is at risk when you cancel the contract for a reason that is not covered by an active contingency — in other words, when you have a change of heart or a life circumstances change that is not addressed by the contract protections you have.

Common situations where earnest money is forfeited:

- Canceling after the inspection period for reasons not related to a contingency

- Failing to apply for financing promptly or in good faith, causing the financing contingency to expire

- Missing the closing date without a legitimate reason or the seller's agreement to extend

- Canceling based on an appraisal if the appraisal contingency was waived in the offer

This is why understanding every contingency in your contract — and the deadlines attached to each one — is so important before you sign. In a situation where a buyer has waived contingencies to make their offer more competitive, the earnest money protection is thinner and the stakes of any decision to cancel are higher.

Earnest Money in Cash Offers

Cash buyers sometimes put down larger earnest money deposits as a signal of commitment in lieu of a financing pre-approval letter. In SWFL's cash-heavy market — particularly in Naples and the luxury segment — earnest money amounts of 5 to 10 percent on cash offers are not uncommon for significant transactions. The logic is straightforward: with no financing contingency, the seller needs confidence that the buyer will perform, and a substantial deposit provides that confidence.

Ready to make your move in Southwest Florida? Let's talk.

Whether you're buying, selling, investing, managing an estate, or just want an honest read on the market — I'm here for that conversation.

Call or text: 727.638.1704

Email: [email protected]

Or reach out at theabreugroup.com

— Daniel

Frequently Asked Questions

Q: Can I put earnest money on a credit card in Florida?

No — earnest money deposits in Florida must be made by check, wire transfer, or other traceable monetary instrument. Credit card payments are not acceptable for escrow deposits. Wire transfer is the fastest and most common method and is what most title companies prefer. Personal checks are acceptable but take longer to clear and can create timing issues.

Q: What happens to earnest money interest while it is in escrow?

In Florida, earnest money held in escrow by a licensed real estate broker must be kept in a non-interest-bearing account unless the parties agree otherwise in writing. Interest-bearing escrow arrangements require explicit agreement from both parties. For most standard residential transactions, the earnest money is held in a non-interest-bearing escrow and the interest question is moot.

Q: Can a seller keep my earnest money if I cancel during the inspection period?

No — if you cancel during the inspection period in compliance with the contract terms, you are entitled to a full refund of your earnest money. The seller cannot keep it. The inspection period cancellation right is one of the buyer's strongest protections in a Florida purchase contract, and exercising it properly — in writing, before the deadline — is what protects the deposit.

Q: What is the difference between earnest money and the down payment?

Earnest money is a good-faith deposit made at the time of contract that goes into escrow. The down payment is the total difference between the purchase price and the loan amount, which is paid at closing. At closing, the earnest money deposit is credited toward the total funds you owe — effectively it becomes part of your down payment. Earnest money is not additional money on top of the down payment; it is an advance portion of it.